Boston Consulting Group Study: The US dollars 300 Billion Reason Why European CEOs Need to Focus on Transformation

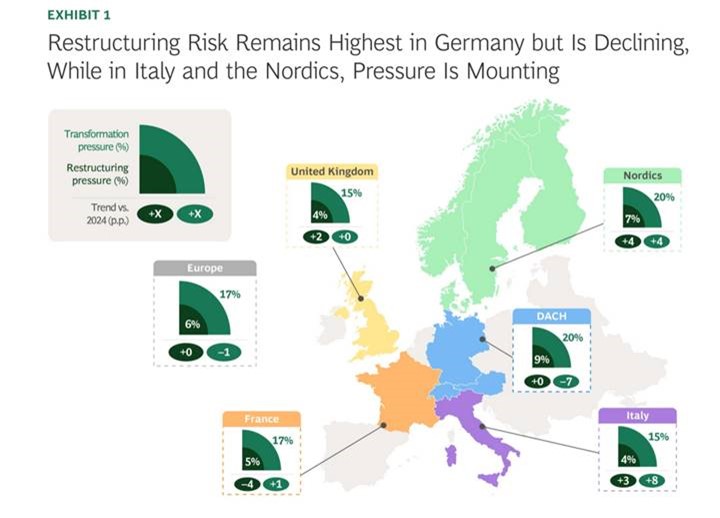

- Of the companies surveyed, 17% are under pressure to transform, and 6% are facing pressure severe enough to require restructuring.

- The good news: Across the continent, inflation, interest rates, and GDP are showing signs of improvement. Bankruptcy rates are stabilizing—up 10% in 2024 from 28% in 2023.

- Germany faces the highest restructuring risk and the second highest pressure to transform. The UK and France are stabilizing.

Trade tensions, geopolitical shocks and tariffs continue to be a major concern for European companies. According to BCG’s third Transformation and Special Situations (TSS) Index, covering 1,700 listed European companies, 17% of companies are under significant transformation pressure and 6% require restructuring. These companies represent over $300 billion of GDP and 3.5 million jobs.

The extended study can be consulted here.

Background and outlook

Transformation and restructuring pressures are driven by weak operational performance and macroeconomic volatility. Geopolitical uncertainty, tariff changes and supply chain disruptions—particularly for energy and grains—have affected costs and delivery times. However, there is also positive news: inflation, interest rates and GDP are showing signs of stabilising, and bankruptcy rates are easing (+10% in 2024 compared to +28% in 2023).

Not all European economies are affected equally – some are facing greater pressures than others

High-risk countries

- Germany: highest restructuring risk and second highest transformation pressure; vulnerable sectors: Consumer Goods & Retail, Chemicals and Automotive.

- Italy and Nordic countries: increasing pressures, driven by Telecom & Technology and Energy.

- UK and France: overall stabilisation, but France still has pressures in Transport & Logistics and Automotive, affecting 489,000 jobs.

Equally, each European sector is feeling pressures differently, and these need to be adapted to the specific context

Key sectors and strategies

- Consumer Goods & Retail: pressures due to reduced discretionary spending and rising operational costs. Recommended measures: portfolio restructuring, price and margin optimization, demand stimulation through AI and effective marketing, integration of sustainability into products.

- Auto: stagnant sales, lower margins, intense competition from China. Recommendations: accelerate innovation (EV and AI), optimize cash flow for R&D investments.

- Chemicals: low demand, increased energy costs and regulations, trade tariffs. Strategies: reduce costs, decarbonize and localize supply chains, sustainably finance the green transition.

- Transportation & Logistics: continued disruption, driver shortage, but air travel and cruise revenues exceeded 2019 levels. Recommendations: diversify and strengthen revenue streams, digitize and automate operations, decarbonize fleets.

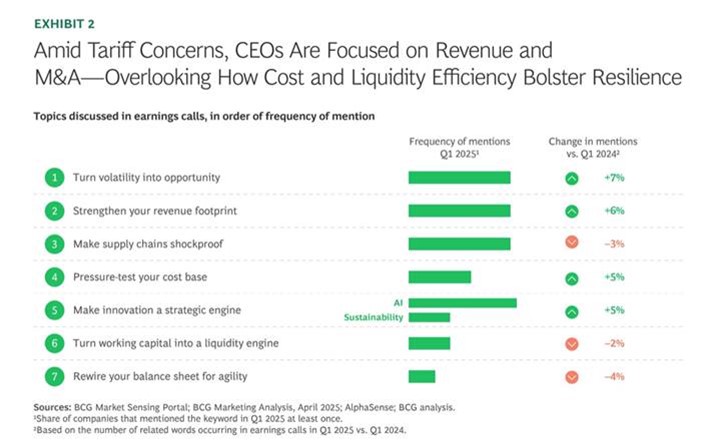

To address risks and turn challenges into opportunities, business leaders must act on multiple fronts simultaneously.

BCG identifies seven key actions to build resilience:

- Turn volatility into opportunity through new demand and M&A.

- Strengthen revenue footprint by adapting prices, products and markets.

- Increase supply chain resilience through regional diversification.

- Test and optimize cost base to protect margins.

- Transform innovation into a strategic driver, with investments in AI and value-creating technologies.

- Leverage working capital for fast and efficient liquidity.

- Reshape balance sheet for agility and smart capital structure.

By implementing these measures, companies in Europe can turn macro risks and sector pressures into competitive opportunities, strengthening their long-term performance and resilience.

Trending Now

You may also like